Last updated on May 26, 2026

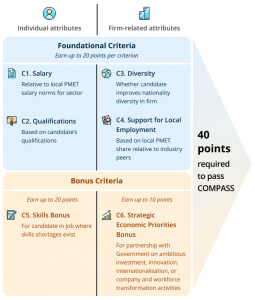

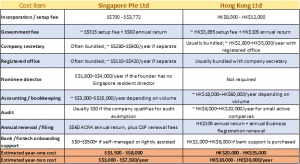

Picture this: you are a Filipino startup founder in the Philippines, and you’re considering setting up an offshore company for a variety of reasons. One being international market access, easier cross-border payments, investor credibility, and tax planning. So the strategic move is to establish an offshore corporate structure that’s not just meant for simple tax planning, but rather for global operational resilience. Legal disclaimer: This guide is for general informational purposes only and should not be treated as legal, tax, or financial advice. Filipino founders should consult a Philippine tax adviser and a licensed corporate service provider before setting up or operating an offshore company. In the Philippines, the two primary destinations for setting up an offshore company are Singapore and Hong Kong. These jurisdictions have different regulatory philosophies. For example, Singapore has doubled down on a “Statutory Anchor” model, emphasizing high-integrity residency requirements and rigorous oversight of corporate service providers through the CSP Act of 2024. So if you’re looking to establish your company in Singapore, you need at least one local resident who will serve as your nominee director, arranged by a registered Corporate Service Provider (CSP). Meanwhile, Hong Kong maintains a “Flexibility-First” approach. As it permits 100% foreign directorship, meaning you don’t need to have a local person as your nominee director. But on the other hand, it enforces a stringent “Audit-for-All.” mandate. This means that all non-dormant companies that are founded and registered in Hong Kong will need to have their financial statements audited annually. This leaves very little room for informal bookkeeping, unlike in previous decades. Instead, you now have to have a practicing CPA registered with the Accounting and Financial Regulatory Council (AFRC) handle your auditing needs. As a Filipino entrepreneur, you have to look at offshore company structures from the perspective of the BIR. Of course, BIR will be interested in these types of setups. One important development is Revenue Memorandum Circular (RMC) No. 024-2026, which clarifies how the BIR applied earlier guidance on the tax treatment of cross-border services after the Aces Philippines case. In simple terms, it gives BIR and taxpayers a framework for assessing whether a cross-border service income shall be treated as Philippine sourced income. The thing is, if the payments from the Philippines and abroad are all routed into an offshore company, that income may appear to sit outside the Philippine tax system. Since the company is technically registered overseas, t he tax issue is not simply where the company is registered. The BIR may examine where the income-producing activities occur, who receives the economic benefit, whether a treaty applies, and whether the offshore company has a taxable presence or Philippine-sourced income. But now, with the Permanent Establishment doctrine, If key management, service delivery, personnel, or income-producing activities are carried out in the Philippines, the offshore structure may create Philippine tax exposure. For Singapore structures, the PH-Singapore tax treaty includes fixed-place PE, service PE, and agency PE concepts that must be reviewed carefully. Depending on the facts, the income may become subject to Philippine tax, including possible taxation of profits attributable to a Philippine PE, withholding tax, VAT, or other applicable tax treatment. Issued on March 30, 2026, RMC No. 024-2026 provides the most current guidance on how the BIR assesses cross-border transactions following the landmark Supreme Court ruling in the Aces Philippines case. This circular clarifies that a mere label of a service as “cross-border” does not automatically render it taxable. Instead, the BIR must now establish four essential elements during an audit to determine whether an international entity has a Permanent Establishment (PE) in the country. Moreover, there’s the 183-day rule. Under the Singapore-Philippines and the pending Hong Kong-Philippines tax treaties, a “Service PE” is one of the most common risks for founders. A service PE is typically triggered if the employees or personnel of the offshore company perform services in the Philippines for an aggregate period exceeding 183 days. Furthermore, BIR Ruling No. ITAD-023-25 emphasized that for the PH-Singapore treaty, the 183-day count is cumulative across the same or connected projects and does not necessarily reset every 12 months. For the burden of proof and audit documentation, under RMC 024-2026, the burden of proof rests squarely on the taxpayer. In a 2026 audit, the BIR accepts certified photocopies of documentation. Founders must maintain a robust “Offshore Defense File.” This includes: With those tax risks in mind, the next practical question is who actually helps founders set up and maintain these offshore structures. This is where Corporate Service Providers, or CSPs, come in. They handle much of the incorporation and compliance work, especially in jurisdictions such as Singapore and Hong Kong, where local residency, nominee directors, and regulatory requirements can shape how the structure operates in practice. Singapore is a well-known offshore hub. Singapore’s reputation as a premier financial hub is, of course, anchored in its adherence to the rule of law and transparency. In 2026, the Accounting and Corporate Regulatory Authority (ACRA) implemented legislative updates to enhance beneficial ownership transparency and professionalize the nominee director industry. Because again, in Singapore, you have to have at least a nominee director based in the country for your offshore company to operate there. For the incorporation and residency requirement, under Section 145 of the Singapore Companies Act 1967, the mandate essentially requires at least one “ordinarily resident” director. In the past, your nominee director could simply be any ordinary Singapore resident—maybe a friend or even someone you met online. By 2026, that has changed. The process used to be much easier, but now you need a CSP to handle it. The minimum requirement is that they should be a Singapore Citizen, a Permanent Resident, or hold an Employment Pass, EntrePass, or Dependant’s Pass. And, of course, there should be a local residential address. For a DP holder, a valid Letter of Consent from the Ministry of Manpower is required. For Philippine-based founders who do not plan to relocate to Singapore immediately, you need to hire a nominee director. But again, they professionalized nominee director services through the CSP Act 2024. So now, starting from June 9, 2025, it is unlawful for any person to act as a nominee director by way of business unless the appointment is arranged by an ACRA-registered Corporate Service Provider. The idea behind this enacted legislation is a response to a 3-billion-dollar money-laundering case in 2024 and 2025, which showed the risks posed by unvetted nominee arrangements. So now, a CSP must conduct a comprehensive “Fit and Proper” assessment of the nominee director candidate. It’s not just a random guy on the street anymore; they must be vetted for fraud history, insolvency, and disqualification under the Companies Act. The liability for failing this assessment is severe for the CSP. A registered CSP that fails to ensure a nominee director is fit and proper may face a fine of up to S$100,000. Currently, when getting a nominee director, it must be facilitated by a registered CSP. The mandatory review vets them for criminal and fiscal responsibility. The nominee director are usually appointed for local-residency compliance and may have limited operational involvement under the service agreement. However, they remain legal directors and retain statutory duties.Their nominee status is visible on the ACRA Business Profile, so they can be validated by anyone, and they must be recorded in the Register of Nominee Directors (ROND). Regarding registry and transparency mandates on the Singapore side, the Companies and Limited Liability Partnerships (Miscellaneous Amendments) Act 2024 tightened transparency requirements. Since June 2025, companies must submit their Register of Nominee Directors (ROND) and Register of Nominee Shareholders (RONS) to ACRA’s central registers. Any changes to the ROND or RONS must be filed with ACRA within two business days. Furthermore, the Register of Registrable Controllers (RORC), which identifies the Ultimate Beneficial Owner, in our case, a Filipino owner holding more than 25% control, must be lodged with ACRA on the first day of incorporation. Moving on to the operational side of registering in Singapore. During the incorporation process on BizFile+, choosing your Singapore Standard Industrial Classification (SSIC) code is a critical operational decision. In 2026, Singaporean banks utilised AI-driven risk assessment tools to flag companies with vague SSIC codes, such as “General Wholesale Trade” or “Management Consultancy.” As of late, banks have been scrutinizing these generic codes more because Singapore is prone to money laundering and fraud. That’s why founders are advised to select specific codes that match their actual business activity. Choosing the appropriate SSIC avoids the bank account registration bottleneck, which can delay account opening for two to six weeks as the banks have to do their KYC and background checks. While technically Singapore has a statutory minimum paid-up capital of just 1 SGD, banks expect initial deposits to range from SGD 1,000 up to SGD 50,000, depending on the business’s risk profile and the founder’s nationality. The exact deposit amount varies by provider. Moreover, let’s talk about transitioning from a nominee director to a founder-director. What if you want to run the business in Singapore, right? This is where the Complementarity Assessment Framework (COMPASS framework) comes in. A Philippine founder who wishes to act as their own resident director must obtain an Employment Pass (EP) to live in Singapore. As of January 1st 2026, an EP applicant must meet updated qualifying salary benchmarks of at least SGD6,200 for financial services, with age-progressive scales for older candidates. Essentially, the older you are, the higher your income should be. Applicants are also assessed under the COMPASS framework, which awards points based on individual qualifications and firm-level attributes. A founder who successfully secures an EP becomes an ordinary resident director. A minimum threshold of at least 40 points is needed to be eligible, while approval time is around three to eight weeks after incorporation. Once your EP and Letter of Consent are approved, that’s the only time the nominee director will resign. With that said, let’s go to Hong Kong. What if you think Singapore is a little bit messy for your liking, with all the corporate stuff and the need to hire a nominee director continuously? In Hong Kong, you don’t have to do that. Hong Kong remains a compelling jurisdiction for Philippine founders due to its “Laissez-Faire” director residency rules and its gateway status to the mainland Chinese market. However, the regulatory tightening in mid-2026 centers on anti-money laundering (AML) protocols and mandatory statutory auditing. Hong Kong law permits a private company limited by shares to have a sole director of any nationality residing anywhere in the world. This provides a significant cost advantage over Singapore in the first year, as it removes the immediate need for a paid nominee director. The mandatory presence in Hong Kong is satisfied through the appointment of a local Company Secretary and the maintenance of a physical registered office address. The Company Secretary must be an individual ordinarily resident in Hong Kong or a corporate entity holding a valid Trust or Company Service Provider (TCSP) license. But on the other hand, there’s a mandatory audit mandate in Hong Kong. The most distinctive feature of Hong Kong compliance in 2026 is that all non-dormant companies must have their financial statements audited annually by a practicing CPA registered with the AFRC. Unlike Singapore, there is no revenue-based exemption from the audit itself. So essentially, even if you’re an active micro-SME, you will need to be fully audited. There is a simplified SME-FRF reporting framework you can follow if your revenue is less than HKD 100 million, but you still have to do it. (subject to eligibility) Dormant entities are exempted if they file for that status, but branch offices or active companies must follow the standard framework. Founders should budget between HKD 8,000 to HKD 30,000 annually for audit and tax filing, depending on transaction volume and the complexity of cross-border intercompany dealings. For TCSP licensing and verification, the Trust or Company Service Provider license is the regulatory bedrock of the Hong Kong virtual office industry. Since 2018, and reinforced in 2026, anyone offering registration and secretarial services by way of business must hold this license. In 2026, there’s an update regarding the “Person Purporting to Act” (PPTA) requirement. TCSPs are subject to AML/CDD requirements, including identifying and verifying persons authorized to act on behalf of corporate customers. This means a Philippine-based owner or manager who is not a director but acts as a contact person must undergo full KYC, including passport scans and utility bills issued within the last three months. The operational interface between a Philippine founder and their offshore entity is managed by the CSP. Currently, there are three commonly used providers: Sleek, Osome, and Statrys. In 2026, they refined their offerings to address the new statutory mandates. (Prices below are indicative as of the time of writing and may change depending on package, promotions, government fees, nominee director requirements, accounting volume, and renewal terms.) Sleek Sleek is focused on growth-stage startups and has transitioned into a comprehensive operating stack for SMEs. Their 2026 strategy is “upfront pricing with no surprises.” For local incorporation in Singapore, it starts at S$700. But for foreign founders, it typically costs around S$2,250 for a basic setup, rising to S$3,650 for full compliance. Sleek offers a “No-Deposit” model for nominee directors, provided the company signs up for their accounting bundle. For Hong Kong, Sleek’s starter tier is HK$6,973. The comprehensive tier costs around HK$10,473. Accounting and tax are bundled in higher tiers for the first year, with renewals based on monthly expenses. Osome Moving on, Osome continues to lead in mobile-first workflows, utilizing heavy automation and AI for bookkeeping and task management. For Singapore, their fully compliant package starts at SGD3,772 per year for foreign founders, which includes a nominee director and registered address. They have a mobile app with real-time chat support and task tracking. In Hong Kong, Osome’s essential tier starts at HK$4,650, which excludes a registered address. Adding one costs HK$3,000 per year. The comprehensive tier is HK$10,650. Their accounting model uses revenue-based pricing, with the”Operate” plan starting at HK$733/m per year for basic bookkeeping. Statrys Next is Statrys. Statrys distinguishes itself by offering an in-house multi-currency business account integrated directly with its incorporation services. For Singapore incorporation, Statrys starts with an all-in package of S$4,095 (or S$3,686 in 2026 promotions), which includes incorporation, one year of a nominee director, a company secretary, and a registered office. For Hong Kong, Statrys offers a standard package of HK$7,740. This covers all government fees, the secretary, and a registered address for year one. Their accounting model uses transaction-based pricing, providing founders with greater control over costs as volume scales. Statrys emphasizes dedicated human support, while other providers may rely more heavily on app-based workflows. For a non-resident Philippine founder, the bank account bottleneck is the single largest point of failure post-incorporation. Traditional banks like HSBC, DBS and Standard Chartered may require more extensive documentation, local substance evidence, and sometimes in-person or video verification. In 2026, many non-resident founders used fintech platforms as an initial operating account because traditional bank onboarding can be slower and document-heavy. Wise Business Its core strength is transparency in FX, using the mid-market exchange rate with no hidden spreads. There are no monthly subscription fees, just a one-time setup fee of S$99 to unlock local account details in 24 currencies. However, it does not support standard Singapore government transfers like CPF contributions or corporate tax payments. Airwallex Business Offered as a “Financial OS,” it provides programmable corporate cards, deep payment gateway integrations, and native multi-currency. There are no account opening fees,and approval is typically granted within days for Hong Kong entities. It also has an AI feature called “Expense Policy Agent” that automatically reviews receipts against company policies. Aspire Business Suitable for Singapore due to its integration with local payment rails such as PayNow, FAST, and GIRO for payroll and tax payments. It also offers a Visa debit card with 1% cashback on common SaaS and marketing spend. For onboarding requirements, under 2026 AML protocols, any Ultimate Beneficial Owner (UBO) holding more than 25% equity must undergo enhanced due diligence. You need identification, like a high-resolution scan of a valid National Passport. Address proof, like a utility bill or bank statement issued within the last 3 months. Source of Wealth (SOW) documentary evidence showing how the initial capital was earned. And a 2-3 page business plan outlining the commercial rationale for using a Singapore or Hong Kong entity, along with expected customers and suppliers. Founders frequently fall into the “Modular Trap” with CSPs, where a low incorporation price leads to unexpected compliance costs in Year 2. While Hong Kong appears cheaper on paper in Year 1 due to the absence of mandatory resident director fees, the TCO typically equalizes with Singapore by Year 2 when accounting for mandatory audit fees and annual Business Registration renewals. Regarding 2026 tax efficiency and incentives, Singapore’s YA 2026 Budget provides a 50% Corporate Income Tax Rebate for active companies, capped at S$40,000. The startup tax exemption also continues to apply, covering up to S$100,000 of normal chargeable income during a company’s first three years. For Hong Kong, the Two-Tiered Profits Tax remains active. The first HKD 2 million of profits is taxed at only 8.25%. Founders claiming the “Offshore Profits Exemption” face 0% tax, but they must provide rigorous proof that all income-generating activities occurred entirely outside of Hong Kong. Global transparency standards are closing in on “hollow” offshore companies. Entities that exist only on paper, with no real management, operations, or commercial purpose, are becoming harder to defend against tax authorities, banks, and regulators. Reputable CSPs in 2026 will refuse to act as a rubber stamp. A professional nominee director in Singapore must be informed of every material decision in a board meeting. If the nominee is treated as a silent placeholder, the BIR may argue that If key decisions, contract negotiation, service delivery, and management are all performed from the Philippines, the BIR may examine whether the offshore company has Philippine-sourced income, a PE, or insufficient offshore substance. Founders must ensure that core business Contracts, board approvals, invoices, service records, and payment flows should be consistent with the company’s actual management and operations. Signing location alone will not cure weak substance. Utilize local payouts via networks like Airwallex or Statrys to ensure transaction trails do not unnecessarily cross Philippine local banks, which would trigger automatic monitoring by the BIR. Record keeping is now essential infrastructure. Hong Kong’s mandate to keep books for at least seven years is now an insurance policy. Contemporaneous logs can be the deciding factor in successfully defending an offshore tax claim against the BIR. Finally, the decision to incorporate offshore in mid-2026 is no longer a binary choice based on cheapness; it’s a multi-layered strategy. Singapore is often better suited for founders seeking investor credibility, ASEAN expansion, stronger regulatory signaling, and possible audit exemption for qualifying small companies. The higher initial cost is offset by the 40% tax rebate, the lack of mandatory audits for micro-SMEs, and the prestige of the ACRA regulatory brand. While Hong Kong Strategy is about “Flexibility.” It is ideal for founders focused on North Asian markets, RMB clearing, and digital nomads who do not wish to deal with resident director requirements. The year-one entry is affordable, but the annual mandatory audit requires a higher level of accounting discipline. For the Philippine Tax Defense, founders must strictly adhere to the elements defined in RMC 024-2026. Material payments to the offshore entity should be supported by contracts, invoices, proof of service delivery, and payment records. By 2026, offshore incorporation had become more documentation-heavy. A defensible structure now requires real governance, clear service records, compliant CSP support, and a tax position backed by evidence. Successful offshore management now requires a fusion of digital compliance tools, professional CSP oversight, and a robust evidence-driven tax strategy. The quality of your corporate setup in Year 1 will determine the survivability of your company in the global tax environment of 2027 and beyond. Accessed Date: May 24, 2026

Why Filipino Founders Consider Offshore Companies

Singapore vs. Hong Kong: Two Different Offshore Models

Philippine Tax Risk: BIR Permanent Establishment Doctrine

Four Elements of Permanent Establishment

Corporate Service Providers and Offshore Compliance

Singapore as an Offshore Hub

Singapore Incorporation and Resident Director Requirements

Nominee Director Rules Under the CSP Act 2024

SSIC Codes, Bank Scrutiny, and Paid-Up Capital

Nominee Director to Founder-Director

Hong Kong as an Offshore Hub

TCSP Licensing and Verification

CSP Comparison

Digital Banking Strategies

2026 AML and Onboarding Requirements

TCO: Singapore vs. Hong Kong

Defending Corporate Substance

Contract Centralization

Final Takeaways

Sources:

https://www.bir.gov.ph/2026-Revenue-Memorandum-Circulars

https://bir-cdn.bir.gov.ph/local/pdf/Singapore%20treaty.pdf

https://bir-cdn.bir.gov.ph/BIR/pdf/PR21MAY2725.pdf

https://www.acra.gov.sg/news-events/news-announcements/865/

https://www.acra.gov.sg/register/corporate-service-provider/checking-if-you-must-register/

https://www.acra.gov.sg/manage/companies/legal-requirements-common-offences/preparing-financial-statements/audit-exemptions/

https://www.iras.gov.sg/taxes/corporate-income-tax/basics-of-corporate-income-tax/corporate-income-tax-rate-rebates-and-tax-exemption-schemes

https://www.mom.gov.sg/passes-and-permits/employment-pass/eligibility

https://www.cr.gov.hk/en/faq/local-company/incorporation.htm

https://www.cr.gov.hk/en/faq/companies-ordinance/co-account-audit.htm

Webpage/docs cited: Significant Controllers Register FAQ

https://www.cr.gov.hk/en/legislation/scr/faq.htm

https://www.cr.gov.hk/en/publications/docs/Guidelines_scr_e.pdf

https://www.gov.hk/en/residents/taxes/taxfiling/taxrates/profitsrates.htm

https://www.ird.gov.hk/eng/paf/bus_pft_tsp.htm

https://sleek.com/hk/resources/company-registration-cost-hong-kong/

https://sleek.com/sg/resources/singapore-corporate-tax/

https://osome.com/sg/incorporation/for-foreigners/

https://statrys.com/hk/company-registration

https://statrys.com/hk/guides/accounting-standards/audit-report

https://wise.com/sg/business/

https://www.airwallex.com/

https://aspireapp.com/🔥 $0.99 NEW Study Guide eBook – Claude Certified Associate – Foundations CCAO-F

Turn Your Team Into Cloud-Ready Professionals Today

Learn AWS with our PlayCloud Hands-On Labs

$2.99 AWS and Azure Exam Study Guide eBooks

New Claude Certified Architect Foundations CCA-F

Learn GCP By Doing! Try Our GCP PlayCloud

Learn Azure with our Azure PlayCloud

FREE AI and AWS Digital Courses

FREE AWS, Azure, GCP Practice Test Samplers

Subscribe to our YouTube Channel

Follow Us On Linkedin